Consolidation loans offer a strategic approach to managing multiple debts efficiently. By consolidating your loans into one, you can simplify your financial obligations and work towards a debt-free future.

Let’s delve into the details of consolidation loans and explore how this financial tool can help you take control of your finances.

What are the steps involved in baking a classic chocolate cake?

To bake a delicious classic chocolate cake, you will need to follow a series of steps including gathering the ingredients, preparing the batter, baking the cake, making the frosting, and decorating it to perfection.

Ingredients for Classic Chocolate Cake

- 2 cups all-purpose flour

- 2 cups granulated sugar

- 3/4 cup unsweetened cocoa powder

- 2 tsp baking powder

- 1 1/2 tsp baking soda

- 1 tsp salt

- 1 cup milk

- 1/2 cup vegetable oil

- 2 large eggs

- 2 tsp vanilla extract

- 1 cup boiling water

Equipment Needed

- Two 9-inch round cake pans

- Mixing bowls

- Whisk or electric mixer

- Spatula

- Cooling rack

Preparing the Cake Batter

- Preheat the oven to 350°F (180°C) and grease the cake pans.

- In a large bowl, combine flour, sugar, cocoa, baking powder, baking soda, and salt.

- Add milk, oil, eggs, and vanilla to the dry ingredients and mix until well combined.

- Stir in the boiling water, the batter will be thin.

- Pour the batter evenly into the prepared pans and bake for 30-35 minutes.

Baking Time and Temperature

Bake the cake at 350°F (180°C) for 30-35 minutes or until a toothpick inserted in the center comes out clean.

Chocolate Frosting

- 1 cup unsalted butter, softened

- 1 1/2 cups unsweetened cocoa powder

- 5 cups powdered sugar

- 2/3 cup milk

- 1 tsp vanilla extract

Decorating and Serving

- Once the cake has cooled, frost it with the chocolate frosting.

- You can add sprinkles, chocolate shavings, or fresh berries for decoration.

- Slice and serve the delicious chocolate cake to enjoy!

Pros and Cons of Consolidation Loans

Consolidation loans can be a helpful tool for managing multiple debts, but they also come with their own set of advantages and disadvantages.

Advantages of Consolidating Loans

- Streamlined Payments: Consolidating multiple debts into one loan means you only have to make one payment each month, simplifying your financial management.

- Lower Interest Rates: Consolidation loans often come with lower interest rates compared to credit cards or other types of loans, potentially saving you money in the long run.

- Improved Credit Score: By paying off multiple debts with a consolidation loan, you can improve your credit score by reducing your overall debt utilization ratio.

- Extended Repayment Terms: Consolidation loans may offer longer repayment terms, resulting in lower monthly payments that are more manageable for your budget.

Drawbacks of Opting for Consolidation Loans

- Additional Costs: Some consolidation loans come with fees or higher interest rates, which could end up costing you more money in the long term.

- Risk of Accumulating More Debt: Consolidating debts may free up credit lines on your existing accounts, tempting you to accumulate more debt if you’re not careful with your spending habits.

- Loss of Benefits: If you’re consolidating federal student loans, you may lose certain borrower benefits like income-driven repayment plans or loan forgiveness options.

Comparison with Other Debt Management Options

- Debt Settlement: Consolidation loans involve repaying the full amount of your debts, while debt settlement typically involves negotiating with creditors to settle for less than what you owe. Debt settlement may negatively impact your credit score, unlike consolidation loans.

- Bankruptcy: While bankruptcy can provide a fresh start by wiping out debts, it has serious long-term consequences on your credit and financial future. Consolidation loans allow you to repay your debts in a structured manner without the same level of impact on your credit.

How to Qualify for Consolidation Loans

Consolidation loans are a great tool for managing multiple debts, but not everyone may qualify for them. Here’s how you can improve your chances of qualifying for consolidation loans.

Eligibility Criteria for Consolidation Loans

- Stable Income: Lenders typically require borrowers to have a stable source of income to ensure they can repay the loan.

- Good Credit Score: A good credit score is often a key factor in qualifying for consolidation loans as it demonstrates your creditworthiness.

- Low Debt-to-Income Ratio: Lenders prefer borrowers with a lower debt-to-income ratio, as it shows they have the capacity to take on additional debt.

- Collateral: Some lenders may require collateral to secure the loan, especially for larger loan amounts.

Tips for Improving Eligibility for Consolidation Loans

- Improve Your Credit Score: Make timely payments, reduce credit card balances, and check your credit report for errors.

- Reduce Debt: Pay off existing debts or at least lower your debt-to-income ratio to make yourself a more attractive borrower.

- Shop Around: Compare offers from different lenders to find the best terms and rates for your consolidation loan.

Role of Credit Scores in Qualifying for Consolidation Loans

Credit scores play a crucial role in determining your eligibility for consolidation loans. Lenders use your credit score to assess your creditworthiness and likelihood of repaying the loan. A higher credit score typically means better chances of qualifying for a consolidation loan with favorable terms and lower interest rates.

Different Types of Consolidation Loans

Consolidation loans come in various forms to cater to different financial situations. Understanding the types of consolidation loans available in the market can help individuals make informed decisions when consolidating their debts.

Secured vs. Unsecured Consolidation Loans

Secured consolidation loans require collateral, such as a home or a car, to secure the loan. These loans typically offer lower interest rates due to the reduced risk for the lender. On the other hand, unsecured consolidation loans do not require collateral but come with higher interest rates to compensate for the increased risk for the lender.

Specialized Consolidation Loans

There are specialized consolidation loans designed to address specific types of debts. For example, student loan consolidation loans are tailored to consolidate multiple student loans into a single loan with a fixed interest rate. Debt management programs also offer specialized consolidation plans to help individuals manage credit card debts more effectively.

Steps to Apply for a Consolidation Loan

When applying for a consolidation loan, it is essential to follow a structured process to ensure a smooth and successful application. Here are the steps you need to take:

Checklist of Documents Required for the Application

- Proof of income: Pay stubs, tax returns, or bank statements

- Identification: Driver’s license, passport, or other government-issued ID

- List of debts to be consolidated: Credit card statements, loan documents, or other relevant information

- Proof of residence: Utility bills, lease agreements, or mortgage statements

- Credit report: To provide a comprehensive overview of your financial situation

Comparing Offers from Different Lenders

- Interest rates: Compare the APR offered by each lender to determine the total cost of the loan

- Repayment terms: Consider the length of the loan and monthly payments to find the most suitable option

- Fees and charges: Look out for any hidden fees or charges that may impact the overall cost of the loan

- Customer reviews: Research the reputation of each lender to ensure they have a track record of good customer service

Consolidation Loans vs. Debt Settlement

When considering options to manage debt, individuals often come across consolidation loans and debt settlement programs. Both options aim to provide relief from overwhelming debt, but they work in different ways and have varying impacts on an individual’s financial situation.

Differences between Consolidation Loans and Debt Settlement

- Consolidation Loans involve combining multiple debts into a single loan with a lower interest rate, making it easier to manage payments. Debt Settlement, on the other hand, involves negotiating with creditors to settle debts for less than what is owed.

- Impact on Credit Scores: Consolidation Loans may have a positive impact on credit scores if payments are made on time, as it shows responsible debt management. Debt Settlement, however, can have a negative impact on credit scores as it involves settling debts for less than the full amount owed.

- Long-Term Financial Implications: Choosing a Consolidation Loan may result in lower interest payments and a more structured repayment plan, while Debt Settlement may lead to a negative mark on credit reports and potential tax consequences for forgiven debt.

Eligibility Criteria and Beneficial Situations

- Consolidation Loans typically require a good credit score and stable income, making it suitable for individuals with manageable debt who want to simplify payments. Debt Settlement programs are generally for individuals with significant debt and financial hardship, who are unable to make full payments.

- Situations where a Consolidation Loan may be more beneficial include having multiple high-interest debts that can be consolidated into a single, lower interest loan, while a Debt Settlement program may be more suitable for individuals with overwhelming debt and limited resources.

Pros and Cons of Consolidation Loans and Debt Settlement

| Consolidation Loans | Debt Settlement |

|---|---|

Pros:

|

Pros:

|

Cons:

|

Cons:

|

Risks Associated with Consolidation Loans

Consolidation loans offer a way to simplify debt repayment by combining multiple debts into a single loan with a lower interest rate. However, there are risks associated with these loans that borrowers should be aware of to make informed decisions.

Potential Risks of Consolidation Loans

- Accruing more debt: Some borrowers may continue to accumulate debt after consolidating, leading to a higher total debt load.

- Extended repayment periods: While monthly payments may be lower, extending the repayment period can result in paying more interest over time.

- Secured loan risks: Opting for a secured consolidation loan puts your collateral at risk if you default on payments.

Mitigating Risks with Consolidation Loans

- Create a budget: Develop a detailed budget to avoid overspending and accumulating more debt.

- Research lenders: Compare offers from multiple lenders to secure the best terms and interest rates.

- Financial counseling: Seek guidance from a financial advisor to ensure consolidation is the right choice for your situation.

Situations where Consolidation Loans may not be the Best Solution

- If you have a low credit score that doesn’t qualify you for a lower interest rate.

- If your total debt amount is not significantly reduced through consolidation.

- If you are unable to commit to making regular payments on the new consolidation loan.

Impact of Credit Score on Consolidation Loans

Your credit score plays a crucial role in determining the approval and terms of a consolidation loan. A higher credit score can help you secure a lower interest rate, while a lower credit score may result in higher rates or even denial of the loan.

Secured vs. Unsecured Consolidation Loans

A secured consolidation loan requires collateral, such as a home or car, to secure the loan. If you default on payments, you risk losing the collateral. On the other hand, unsecured consolidation loans do not require collateral but typically come with higher interest rates.

Consequences of Missing Payments on a Consolidation Loan

Missing payments on a consolidation loan can lead to late fees, increased interest rates, and a negative impact on your credit score. It is essential to make timely payments to avoid further financial repercussions.

Calculating the Total Cost of a Consolidation Loan

To calculate the total cost of a consolidation loan, add the total amount of the loan, including any fees, and multiply it by the interest rate over the loan term. This will give you a clear picture of how much you will pay in total.

Consolidation Loans for Different Financial Situations

Consolidation loans are a financial tool that can help individuals manage and streamline their debts more effectively. By combining multiple debts into a single loan with one monthly payment, borrowers can simplify their repayment process and potentially lower their overall interest rates.

Step-by-Step Guide on Applying for a Consolidation Loan

- Check your credit score and gather necessary financial documents such as income statements, debt information, and identification.

- Research different lenders and loan options to find the best fit for your financial situation.

- Submit a loan application with the required documents and wait for approval.

- If approved, review the terms and conditions of the loan carefully before signing any agreement.

Pros and Cons of Different Types of Consolidation Loans

| Consolidation Loan Type | Pros | Cons |

|---|---|---|

| Secured Loan | Lower interest rates | Risk of losing collateral |

| Unsecured Loan | No collateral required | Higher interest rates |

Comparison with Other Debt Relief Options

Debt consolidation focuses on combining multiple debts into one, while debt settlement involves negotiating with creditors to pay off debts for less than what is owed. Bankruptcy is a legal process that can discharge debts but has long-term financial consequences.

Tips for Negotiating Better Loan Terms

- Highlight your creditworthiness and positive payment history to lenders.

- Shop around and compare offers from multiple lenders to leverage better terms.

- Negotiate for lower interest rates or flexible repayment terms based on your financial situation.

A financial expert advises, “Always carefully review the terms and conditions of a consolidation loan to ensure it aligns with your financial goals and capabilities.”

Impact of Consolidation Loans on Credit Scores

When considering consolidation loans, it is crucial to understand how they can affect your credit score. Let’s delve into the factors that determine these impacts and explore the differences between various types of consolidation loans.

Factors Affecting Credit Scores with Consolidation Loans

- Payment History: Timely payments on the new consolidated loan can positively impact your credit score.

- Credit Utilization: Lowering your overall credit utilization through consolidation can improve your credit score.

- Credit Mix: The variety of credit accounts, including the consolidated loan, can influence your credit score.

- Hard Inquiries: Applying for a new consolidation loan may result in a temporary dip in your credit score due to hard inquiries.

Differences in Credit Score Effects between Loan Types

- Balance Transfer: Transferring high-interest credit card balances to a new card can impact credit utilization and potentially improve your score.

- Personal Loans: Taking out a personal loan for consolidation may affect credit mix positively if it adds installment debt to your profile.

- Home Equity Loans: Using home equity for consolidation can have a significant impact on credit scores, as it involves securing debt with collateral.

Calculating Potential Credit Score Impact

Before opting for a consolidation loan, calculate the potential impact on your credit score by considering factors like payment history, credit utilization, and credit mix.

Timeline for Credit Score Improvements

- Immediate Impact: Changes in credit scores may be noticeable shortly after consolidating loans due to reduced credit utilization.

- Long-Term Improvements: Consistent, on-time payments on the new loan can lead to gradual credit score improvements over time.

Credit Score Changes Post-Consolidation

- High Debt Levels: Individuals with high levels of debt may see a more significant increase in credit scores post-consolidation due to lower credit utilization.

- Low Debt Levels: Those with minimal debt may experience a smaller credit score change but can still benefit from a more diverse credit mix.

Alternatives to Consolidation Loans

When considering debt management strategies, there are alternatives to consolidation loans that may better suit your financial situation. Here, we explore some other options.

Debt Snowball vs. Debt Avalanche

Two popular methods for paying off debt are the debt snowball and debt avalanche approaches. The debt snowball method involves paying off your smallest debts first, while the debt avalanche method focuses on tackling debts with the highest interest rates first.

Debt Consolidation Loans vs. Debt Management Plans

Debt management plans are another alternative to consolidation loans. These plans involve working with a credit counseling agency to negotiate lower interest rates and monthly payments with your creditors. While consolidation loans involve taking out a new loan to pay off existing debts, debt management plans focus on creating a structured repayment plan.

| Eligibility Criteria | Consolidation Loans | Debt Settlement Programs |

|---|---|---|

| Credit Score Requirement | Good to Excellent | Lower Credit Score Accepted |

| Debt Amount | High Debt Amounts | Debt Settlement Programs |

| Interest Rates | Lower Interest Rates | Interest Negotiation |

Financial experts caution that consolidation loans may not address the root cause of debt accumulation and could lead to a false sense of security, potentially resulting in even higher debt levels.

Consolidation Loans for Different Types of Debt

When it comes to consolidating debt, different types of debt require specific considerations to optimize the process and achieve financial goals effectively.

Credit Card Debt

- Consolidation loans can be used to combine multiple credit card balances into a single, more manageable payment.

- Consider the interest rate on the consolidation loan compared to the rates on the credit cards to ensure savings in the long run.

- Avoid accumulating new credit card debt after consolidating to prevent further financial strain.

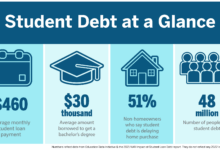

Student Loans

- Consolidating student loans can simplify repayment by combining multiple loans into one monthly payment.

- Explore options for federal student loan consolidation or private consolidation based on individual circumstances.

- Understand any potential loss of borrower benefits or repayment options when consolidating federal student loans.

Medical Bills

- Using a consolidation loan for medical bills can help streamline payments and avoid high-interest medical credit cards.

- Negotiate with healthcare providers for possible discounts or payment plans before consolidating medical bills.

- Ensure that the total amount of medical debt included in the consolidation loan is manageable within the budget.

Common Mistakes to Avoid When Consolidating Loans

Consolidating loans can be a beneficial financial move, but it’s essential to avoid common pitfalls that could lead to unfavorable outcomes. Here are some tips on navigating the consolidation process effectively and ensuring a successful loan consolidation:

Not Reviewing Terms and Conditions Thoroughly

- Before agreeing to a consolidation loan, make sure to carefully review the terms and conditions to understand the interest rates, repayment terms, and any associated fees.

- Skipping this step can lead to unexpected costs and obligations that may not align with your financial goals.

Missing Payments and Credit Score Impact

- Missing payments on a consolidated loan can have a negative impact on your credit score, making it crucial to prioritize timely repayments.

- A lower credit score can affect your ability to secure future credit or loans at favorable terms.

Comparing Different Loan Offers

- It’s important to compare different consolidation loan offers to choose the most beneficial option in terms of interest rates, repayment terms, and overall cost.

- Failure to shop around and compare offers can result in higher costs and missed opportunities for better terms.

Understanding Total Cost and Creating a Budget Plan

- Ensure you understand the total cost of the consolidated loan, including all interest rates and fees, to avoid any surprises down the line.

- Creating a budget plan can help you manage your finances effectively, make timely payments on the consolidated loan, and avoid further financial strain.

Factors to Consider Before Consolidating Loans

Before consolidating loans, it is crucial to carefully evaluate various factors to make an informed decision that aligns with your financial goals and situation. Here are key considerations to keep in mind:

Assess Current Debts and Financial Situation

- Evaluate the total amount of debt you currently have, including interest rates and repayment terms.

- Understand your monthly budget and income to determine how much you can afford to pay towards a consolidated loan.

Impact on Credit Score

- Consider how consolidating loans may affect your credit score, as opening a new account can temporarily lower your score.

- Ensure that timely payments on the consolidated loan can help improve your credit over time.

Comparison of Repayment Options

- Compare the interest rates and repayment terms of your current loans with potential consolidated loan options to assess potential savings.

- Evaluate if a lower interest rate or longer repayment term will benefit your financial situation in the long run.

Professional Financial Advice

Seeking advice from a financial advisor or credit counselor can provide valuable insights and guidance in making the right decision to consolidate loans.

Consolidation Loans and Financial Wellness

Consolidation loans play a crucial role in promoting financial well-being by helping individuals streamline their debt repayment process and manage their finances more effectively. By consolidating multiple debts into a single loan with a lower interest rate, borrowers can reduce the total amount of interest paid over time and simplify their monthly payments.

Benefits of Consolidation Loans for Financial Wellness

- Consolidation loans can help individuals better organize their finances by combining multiple debts into one manageable payment.

- Lower interest rates on consolidation loans can lead to reduced overall debt burden and potentially save money in the long run.

- Having a single monthly payment can make budgeting easier and reduce the risk of missed or late payments.

- Consolidation loans can provide a sense of relief and control over one’s financial situation, leading to reduced stress and anxiety.

Tips for Using Consolidation Loans for Financial Wellness

- Before applying for a consolidation loan, carefully assess your current financial situation and create a realistic repayment plan.

- Compare different consolidation loan options to find the best terms and interest rates that suit your needs.

- Avoid taking on additional debt while repaying a consolidation loan to prevent falling back into a cycle of financial instability.

- Consider seeking financial counseling or advice to develop healthy financial habits and strategies alongside using a consolidation loan.

Future Trends in Consolidation Loans

Consolidation loans have been a popular option for individuals looking to simplify their debt repayment process and potentially save money on interest rates. As we look towards the future, several trends are expected to shape the consolidation loan industry.

Innovations in Technology

With advancements in technology, we can expect to see more streamlined and efficient processes for applying for and managing consolidation loans. Online platforms and mobile apps may make it easier for borrowers to access information, compare loan options, and make payments.

Personalized Loan Options

In the future, consolidation loan providers may offer more personalized loan options tailored to individual financial situations. This could include flexible repayment terms, customized interest rates, and specialized programs for specific types of debt.

Impact of Economic Trends

Economic trends, such as changes in interest rates, inflation, and unemployment rates, can have a significant impact on the demand for consolidation loans. As the economy fluctuates, borrowers may turn to consolidation loans as a way to manage their debt more effectively.

Expansion of Online Lenders

Online lenders have been gaining popularity in the lending industry, and this trend is likely to continue in the consolidation loan market. Borrowers may have access to a wider range of loan options from online lenders, potentially leading to increased competition and more favorable terms.

Focus on Financial Education

In the future, there may be a greater emphasis on financial education for borrowers considering consolidation loans. Lenders and financial institutions may provide resources and tools to help individuals make informed decisions about their debt management strategies.

Final Thoughts

In conclusion, consolidation loans serve as a valuable tool for individuals looking to streamline their debt and improve their financial well-being. By understanding the intricacies of consolidation loans, you can make informed decisions to secure a more stable financial future.